If natural gas supplies from Russia were to be completely cut off from May 1, Europe would have to reduce its consumption by a total of 790 TWh over the next twelve months. This is the result of the brief analysis “Impact of missing gas supplies from Russia on Security of Supply” by the Institute of Energy Economics (EWI) at the University of Cologne. If the storage facilities are to be completely emptied by April 30, 2023, demand for natural gas would have to be reduced by a total of 459 TWh.

Currently, the EU obtains 30 percent of its natural gas imports from Russia (as of Q1 2022), while Germany obtains 35 percent (as of May 2, 2022). In addition to its own production and imports from Russia, the EU has four major import corridors for natural gas: Azerbaijan, Algeria, Libya and Norway also supply the EU via pipelines. In addition, liquefied natural gas (LNG) can be imported via the global gas market, assuming the appropriate infrastructure is available.

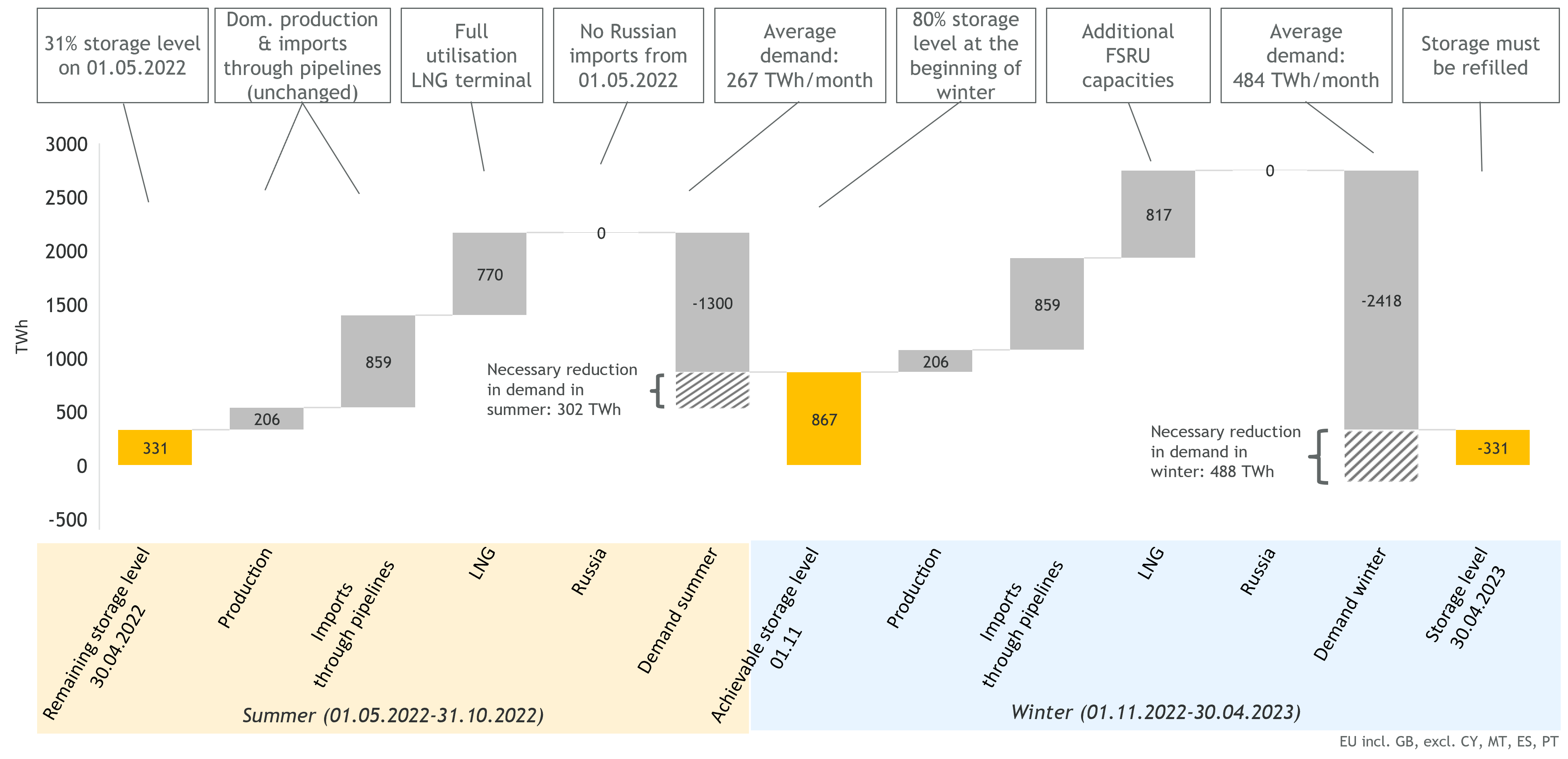

Aggregated, the EU’s storage facilities are currently 33 percent full (as of April 30, 2022). To ensure security of supply in the winter of 2022/2023, storage facilities must be filled to a high level. Other factors are also important for supply security:

“In sum, this means that if gas supplies from Russia are completely absent, even in the optimal case, i.e., with maximum LNG imports and maximum inflows from non-Russian pipelines, the available volumes in summer are unlikely to be sufficient to both fill storage and meet the remaining demand,” said Dr. Eren Çam, manager at EWI.

“This would leave policymakers with the dilemma of balancing between serving summer demand (mainly industry, power and hot water) and safeguarding winter demand (additional demand mainly for space heating). A reduction in gas demand over the summer should therefore be initiated immediately, and winter demand reduced with foresight, if security of supply is to be secured constantly.”

In addition, under the new German Gas Storage Act, German storage facilities must be at least 90 percent full by Nov. 1, 2022; the EU Commission proposes a minimum of 80 percent for European storage facilities by Nov. 1. Such requirements would bring forward part of the supply gap to the summer and reduce the gap in the winter accordingly. A European level requirement of 80 percent by Nov. 1, 2022, would result in a gap of 302 TWh (18 percent of summer demand) in summer, while the gap in winter would drop to 488 TWh (17 percent of winter demand). If storage were to be completely emptied, a reduction of 157 TWh (5 percent of winter demand) would be necessary.

Reaching these fill levels to back up winter demand would be in volume competition with the remaining summer demand. Aware of this target, other market players might only provide the needed volumes for prices far above the prevailing market price. “The targeted level of storage fill targets should therefore be kept under review in light of further geopolitical developments,” Çam says.

In the scenario, researchers considered gas flows in the European Union (EU) and the United Kingdom on a balance sheet basis; infrastructure bottlenecks are not considered. The Iberian Peninsula is also not considered, as it is only marginally connected to the European gas grid. The assumed demand volumes are taken from the reference scenarios of the ENTSOG Supply Outlooks.