The Institute of Energy Economics at the University of Cologne (EWI) has examined the development of prices for the energy carriers natural gas, oil, hard coal and electricity for the years 2026 and 2030 in several scenarios. The electricity and gas demand, the availability of Russian imports and the expansion of renewable energies are varied. The development of gas prices in Europe depends on the volume of energy imports from Russia and the development of gas demand. If gas demand can be reduced significantly and imports are at least partially available, gas prices could fall back to around historic levels by 2030. If gas demand cannot be reduced, gas prices would remain above that level in 2030. Wholesale electricity prices are significantly above historical prices in the medium term in all scenarios.

This is shown by the EWI report “Szenarien für die Preisentwicklung von Energieträgern” commissioned by the academy project “Energiesysteme der Zukunft” (ESYS). The EWI report forms a basis for the impulse paper “Welche Auswirkungen hat der Ukrainekrieg auf die Energiepreise und Versorgungssicherheit in Europa?“.

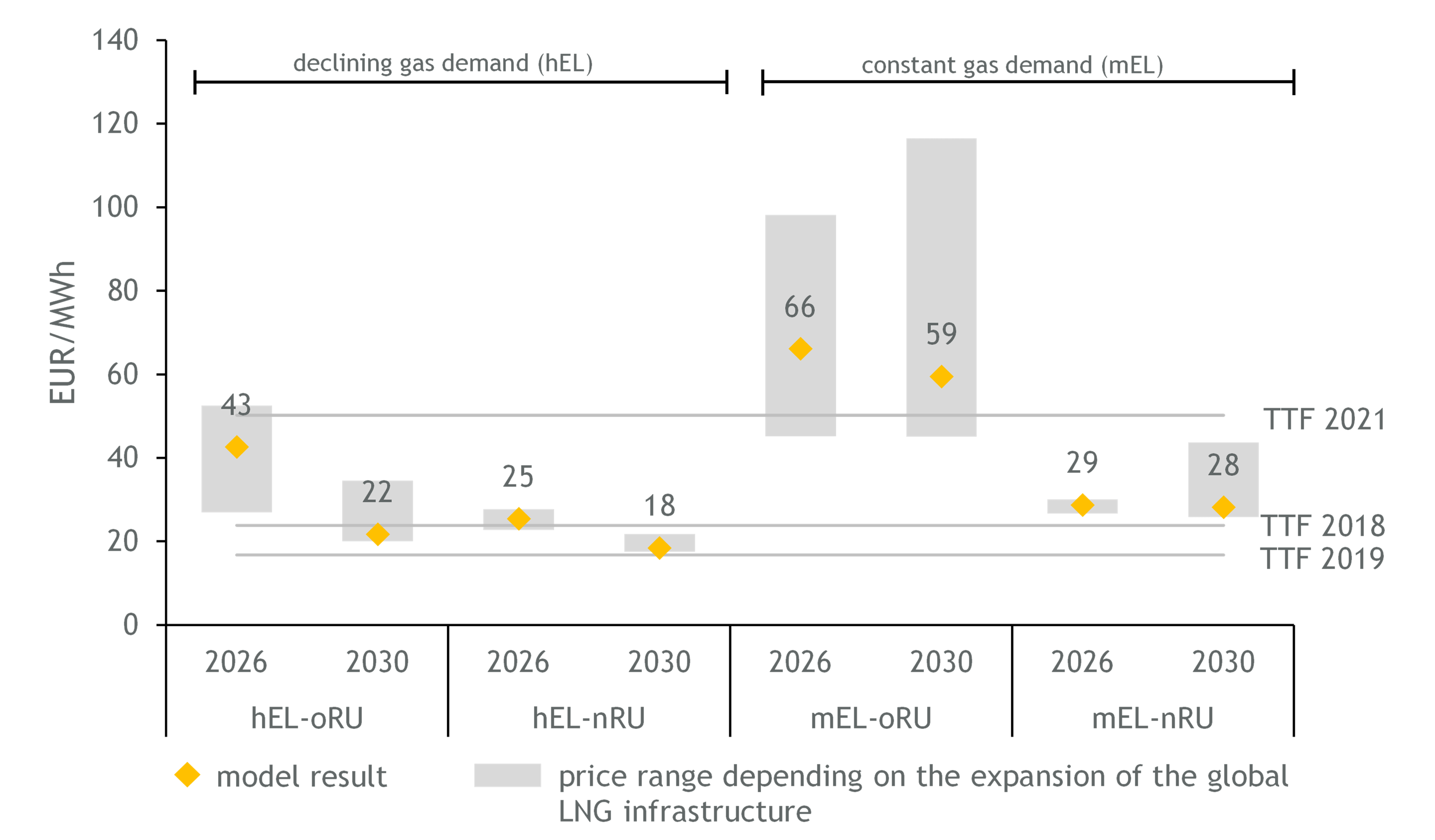

If gas demand declines by about one-third by 2030, prices of 25-43 EUR/MWh in 2026 and 18-22 EUR/MWh in 2030 could emerge. These would be roughly in line with representative historical gas prices (∅ 2018 around 24 EUR/MWh). If gas demand remained constant, prices could remain at high levels of 29-66 EUR/MWh in 2026 and 28-59 EUR/MWh in 2030. Without gas imports from Russia, the upper values of the range are reached. If Russian imports are halved compared to 2021, prices could fall to the lower end. “Without Russian imports, the share of LNG from the U.S. could rise to as much as 35 percent of European imports by 2030 due to high investments in liquefaction facilities. The U.S. would play a central role in supplying Europe also in the future,” says Eren Çam, manager at EWI.

Russia can only partially compensate for the loss of exports to the European market by expanding its exports to the Asian market. In all scenarios, the total volume of Russian gas exports is lower than in 2021. In the scenarios without Russian imports for Europe, exports decline by up to 55 percent by 2030, and by up to 33 percent in the scenarios with low availability of Russian imports.

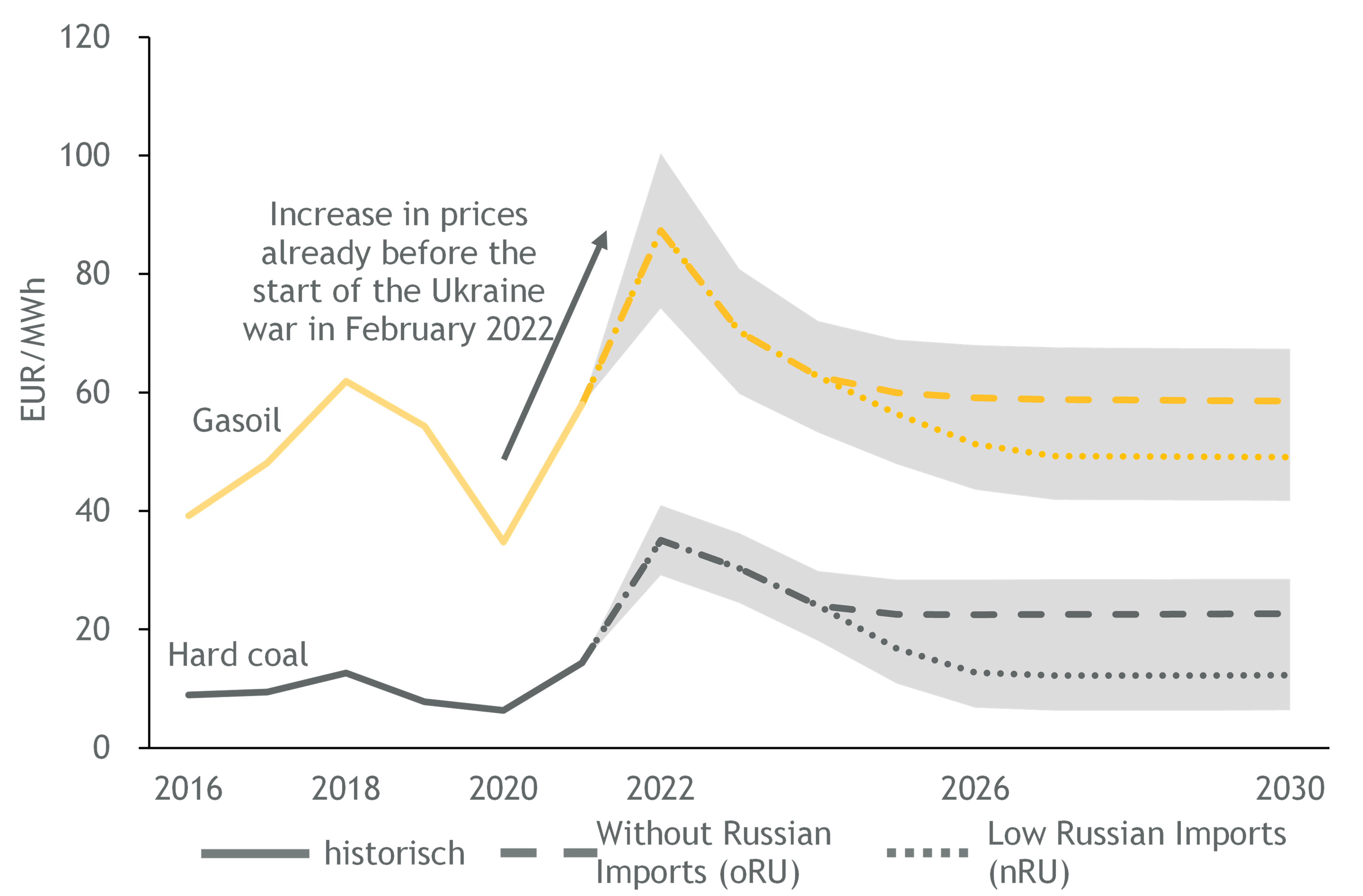

With regard to oil, prices could decline significantly after a price peak in 2022. In the scenario without Russian imports, the price falls to a level in the upper range of historical wholesale prices by 2026 (oil = ∅ 2016 to 2021 approx. 50 EUR/MWh and hard coal = ∅ 2016 to 2021 approx. 10 EUR/MWh). In the case of partial availability of Russian oil imports, the price level falls to about the historical average. Possible reasons for this decrease are the lower imports from Russia compared to gas and hard coal, which means that the adjustment of the import structure is lower. Furthermore, OPEC has already announced that it will increase production capacities.

The possible development of coal prices also shows that prices will fall. However, if there are no more imports from Russia in the medium term, the price level will be higher than the historical price level. This is due, among other things, to the increase in transport distances from the USA, Colombia, and South Africa. A partial availability of Russian coal imports leads to a drop in prices in the scenario accordingly. In this case, the price falls to a level in the upper range of historical values.

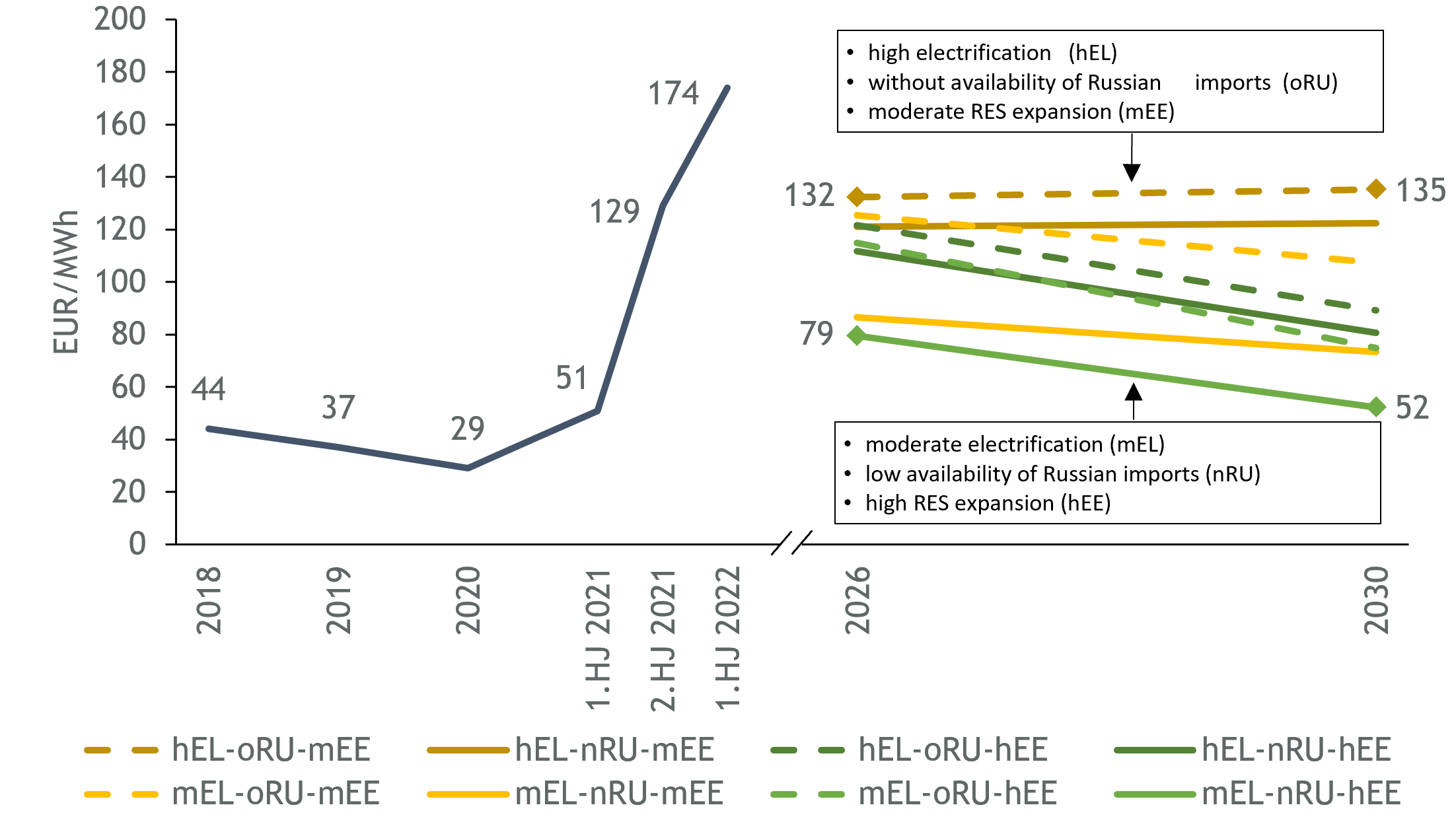

The price developments for natural gas and hard coal have a major impact on the electricity market. In all scenarios, there is a significant increase in prices compared to the long-term historical wholesale prices (∅ 2016 to 2019 approx. 37 EUR/MWh). Compared with the current high prices (∅ 1st half of 2022: ∅ 174 EUR/MWh), there is a clear decrease. The highest annual average prices of up to 132 EUR/MWh (2026) and 135 EUR/MWh (2030) result in the scenarios in which price-increasing effects overlap: a strong increase in electricity demand, no availability of Russian energy source imports, and a moderate expansion of renewable energies. The lowest prices, at 79 EUR/MWh (2026) and 52 EUR/MWh (2030), occur in the opposite case, i.e., with a moderate increase in electricity demand, low availability of Russian imports, and an expansion of renewables in line with the German government’s ambitious targets. “The expansion of renewable energies is an essential lever for a medium-term

decline in wholesale electricity prices,” says Max Gierkink, manager at the EWI.

Energy price increases are a particular burden on players such as (low-income) households and (energy-intensive) industries. In industry, energy-intensive sectors from the basic materials industry are particularly affected. “In the medium term, high energy prices in Europe will create competitive disadvantages compared with other regions such as Asia or the USA. Our analysis shows that, for example, the competitive position of gas-intensive basic industries such as the German fertilizer industry could deteriorate compared to Asia and especially the U.S.,” says Max Gierkink, manager at EWI. “Energy-intensive industries could thus have an incentive to relocate their production sites.”

On the household side, low-income households have been hit hard by energy price increases. This is due, among other things, to the rising share of disposable income spent on energy or low adjustment options through investments in efficient heating technologies, photovoltaic systems or building renovation.