In 2023, fuel prices fell and there were more conventional power plants on the electricity market. The fact that more conventional power plants participated in the market was in contrast to the downward trend of previous years. This was due to legal requirements that prevented the decommissioning of coal-fired power plants and brought existing power plants from the reserves to the market as so-called “Marktrückkehrer” (market returnees).

These are the key findings of the analysis “Development of conventional power plant capacities on the German electricity market” by the Institute of Energy Economics at the University of Cologne (EWI). The analysis by Dr. Fabian Arnold, Jakob Junkermann and Martin Lange is based on the EWI Merit-Order Tool 2023, which is now available free of charge on the EWI website. The EWI Merit-Order Tool can be used to visualize the average deployment sequence of conventional power plants in Germany based on their marginal costs. The deployment sequence, the so-called merit order, is a central component of price formation on electricity exchanges: The most expensive power plant required to cover demand in each hour determines the price for all market participants, i.e. it sets the price.

Significant changes compared to the merit order for 2022 are distinguishable. “Two effects can be observed this year: Firstly, lower gas and coal prices led to a flatter merit order curve. Secondly, the so-called market returnees have increased the total power plant capacity available on the market,” says Dr. Fabian Arnold. “The flatter merit order curve means that the marginal costs of the various power plant technologies have converged.”

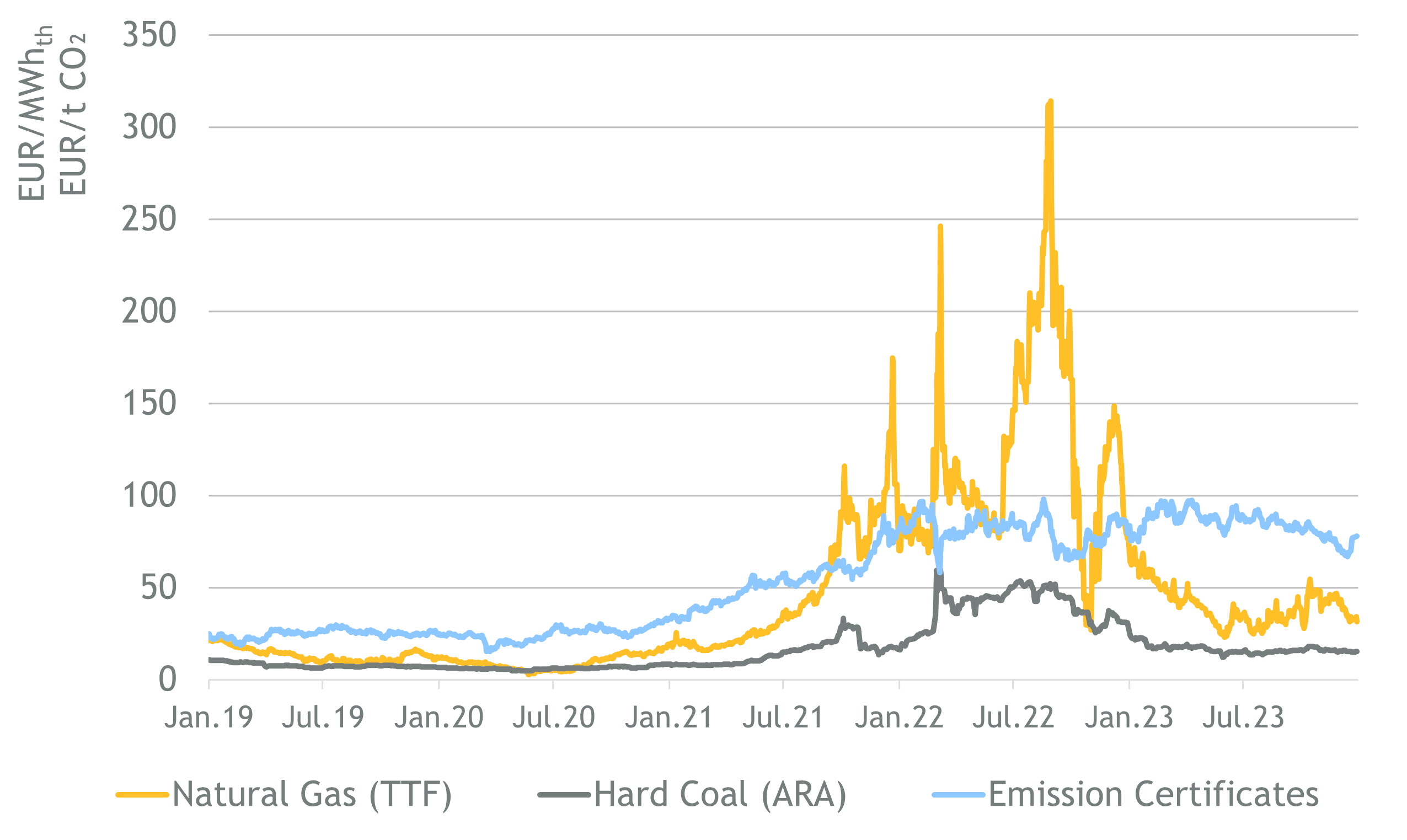

Prices for conventional fuels fell again in 2023. Natural gas cost 67% less on average in 2023 than in the previous year. Hard coal was around 58 percent cheaper. The price of emission certificates remained roughly the same (+4%). As a result of the price falls, more gas-fired power plants had once again similar marginal costs as their coal-fired counterparts.

The additional conventional power plants on the market returned to the electricity market for a limited period in 2022 and 2023 as part of the Substitute Power Plant Provision Act (Ersatzkraftwerkebereithaltungsgesetz). These were mainly lignite and hard coal-fired power plants from existing reserves. In addition, shutdowns of coal-fired power plants that were plant to be taken off the grid in 2022 and 2023 as part of the German coal phase-out were postponed. With the expiry of the Substitute Power Plant Provision Act, these market returnee power plants are due to leave the electricity market again at the end of March 2024.

“In the coming years, a further decline in conventional generation capacities on the electricity market is expected, as further coal-fired power plants also leave the market due to the coal phase-out,” says Arnold. At the same time, demand for electricity and peak loads could increase, for example due to the electrification of heating and transportation. “The loss of power plant capacities could be compensated for, for example, by the addition of new generation capacities such as renewable energies, H2-ready gas-fired power plants, increased European market integration and the expansion of flexibility and storage.”