The generation of electricity from gas is to be reduced in Germany, while continuing to guarantee security of supply. While the German government decided in October 2022 to allow coal and oil-fired power plants to return to the market for a limited period and to extend the operation of three German nuclear power plants until mid-April 2023, some French nuclear power plants are not available for power generation for technical reasons. Their return to the market is subject to uncertainty.

How European gas-fired power generation and German electricity prices (marginal costs) from November 2022 to April 2023 are related to the availability of French and German nuclear power plants and what effects might result is shown in the analysis “Gas-fired Power Generation in Winter 2022/2023” prepared by the Institute of Energy Economics at the University of Cologne (EWI) on behalf of the Society for the Promotion of the Institute of Energy Economics at the University of Cologne e.V.

For the analysis, an EWI team consisting of Dr. Johannes Wagner, Dr. Philip Schnaars, Nils Namockel, Hendrik Diers and Julian Keutz modeled the European electricity market from November 1, 2022 to April 30, 2023 in three different scenarios using the EWI’s proprietary model DIMENSION. In these, the factors of extended power operation of the three German nuclear power plants until mid-April 2023 and the availability of electricity imports from France, which in turn depends on the availability of French nuclear power plants, are varied. All three scenarios consider the German government’s plans to reactivate or continue operating German coal and oil-fired power plants. The future development of commodity prices in the scenarios is based on market-traded long-term supply contracts.

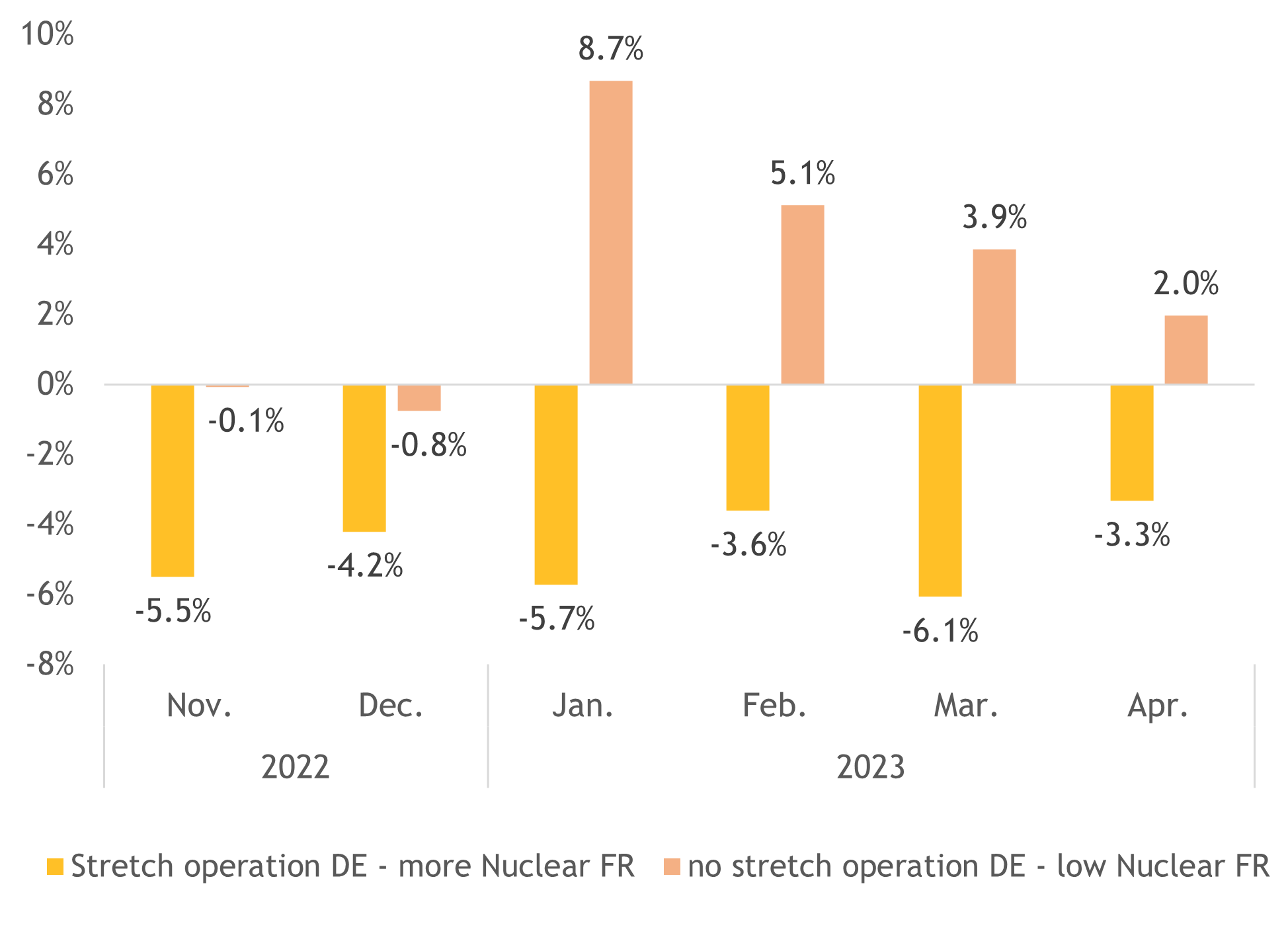

The analysis shows that a resumption of higher electricity generation in France could reduce electricity prices in Germany – measured by the change in marginal costs of electricity generation – by around 3 to 5 percent on a monthly average. This would reduce net exports of electricity from Germany by around 20 percent.

For the politically approved extended power operation of the three German nuclear power plants, the analysis shows a slight dampening effect on the calculated marginal costs of electricity generation of three percent on average; the effect is highest in January (nine percent) and decreases continuously over the remaining winter months and the expiring stretch operation. Without the extended power operation, net exports would be reduced by 60 percent.

In the model, this difference can be explained by the fact that in the scenario without the politically decided extended power operation, more electricity would have to be imported from fossil power plants, especially abroad, since the German replacement power plants are already operating close to maximum capacity. In the scenario with extended power operation, Germany provides more electricity at low marginal costs, much of which is exported to its European neighbors in the model. In contrast, the increase in the availability of French nuclear power has a volume effect primarily in France, where it replaces fossil-fuel power generation with natural gas.

The analysis also calculates the impact on European gas demand. In particular, higher power generation in France could lead to savings here. With the assumptions calculated in the study, there would be a reduction potential of 49 TWh of natural gas in Europe for the six months considered, which corresponds to just under one tenth of the annual capacity of the Nord Stream 1 natural gas pipeline or about three shiploads of an average LNG tanker. The effect of extended power operation on European gas demand is estimated to be significantly lower at 8 TWh.